To keep your household finances in order, you need to know how to create a family budget.

Here, we’ll show you how to do so.

Specifically, we’ll go over what a family budget is, why their a good idea, and how to easily create and maintain a one.

Personally, a budget has been an excellent tool for my family. Once we started tracking our finances, we could save enough to buy three houses outright and skyrocket our financial independence goal to 40 years of age.

So if you are interested in seeing how a family budget can help you tame your spending habits, or even allow you to achieve the life of your dreams, check out the easy read below.

Let’s dive right in.

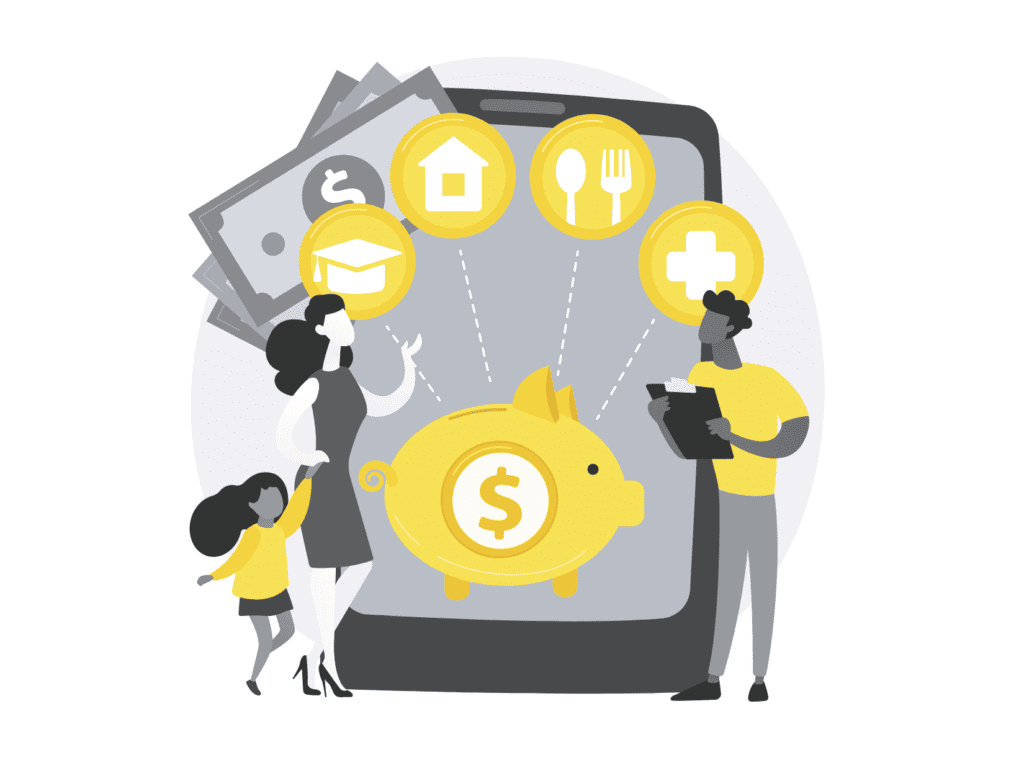

What Is Family Budget Planning?

A family budget is a spending and savings plan that helps you track spending by allocating money for all of the necessary expenses a family has, such as housing, food, healthcare, transportation, and education. A family budget also includes money for savings and debt repayment.

Why Is It A Good Idea For The Family To Save Money?

There are several reasons why it’s a good idea for the family to save more money.

One of the most important is that it can help to protect the family’s income. If something unexpected happens, like your regular take-home pay stops coming because of an injury, the family may need to rely on their savings to make ends meet.

Additionally, saving money can help the family afford a big purchase, such as a home or a new car, which can also be used for emergencies, and help you avoid lifestyle inflation or even the effects of a high cost of living.

Finally, by saving money, the family can help to ensure their financial security in the future.

How Do You Create A Family Budget?

1. Choose Softcopy or Hardcopy

There are a few different ways that you can go about creating a family budget. You can either opt for a softcopy or write a hardcopy budget.

Both have their pros and cons that you will need to consider before deciding.

So, what are the differences between a softcopy and a hardcopy budget?

A softcopy budget is one you create using software, such as Microsoft Excel or Google Sheets.

The advantage of a softcopy budget is that it is easy to update and change as your circumstances change. You can also access your softcopy budget from anywhere if you have an internet connection.

The downside of a softcopy budget is that it can be easy to lose track of if you don’t keep it well-organized.

Additionally, if your computer crashes or you lose your phone, you could lose all your budgeting data.

A hardcopy budget is one that you create using a physical notebook or a printed-out spreadsheet.

The advantage of a hardcopy budget is that it is much harder to lose track of. You can also make changes to a hardcopy budget more quickly than a softcopy budget.

The downside of a hardcopy budget is that it can be more challenging to update, and you will need to have access to a printer if you want to make changes.

Additionally, it can be difficult to find if you misplace your hardcopy budget.

So, which type of budget should you choose?

Ultimately, the decision comes down to personal preference. If you like the idea of accessing your budget from anywhere, a softcopy budget might be the best choice for you. If you prefer the simplicity of a physical notebook, a hardcopy budget might be the way to go.

Whatever you decide, the most important thing is that you find a budgeting method that gets your family on the same page so that you can stick to it.

2. Document Your Income

Now that you’ve chosen the type of budget you will use, it’s time to start documenting your income. This is an essential step in creating a budget, as your income will dictate how much money you have to work with each month.

There are a few different ways that you can document your income. The first is to write down your monthly income from each source. This could include your salary, freelance work, child support, or alimony.

If you have a more complex income situation, you may want to use budgeting software to track your income. This can be helpful if you have multiple income sources or if your income fluctuates from month to month.

Free budgeting apps like Personal Capital are a great choice if you’re looking for a simple way to manage your finances, no matter how simple or complex. They even offer free analysis from professionals to help you build financial plans suited to your unique situation.

(It’s kind of like your own little pocket financial institution. 😁)

Once you have a good understanding of your monthly income, you can allocate it towards different expenses.

3. Document Discretionary and Fixed Expenses

The next step in creating a budget is to document your discretionary and fixed expenses.

Discretionary expenses fluctuate from month to month, such as entertainment or dining out.

Fixed expenses stay the same each month, such as rent, utility bills, child care, and a car payment.

Once you have a good understanding of your monthly expenses, you can start to allocate your income toward them.

It’s essential to be realistic when budgeting for your expenses. For example, if you know that you tend to spend a lot on entertainment, don’t budget a small amount for it. Likewise, don’t budget a significant amount if you have a low fixed expense like rent.

The goal is to create a budget that you can stick to. However, suppose you find that your budget is too restrictive. In that case, you may want to consider increasing your income or finding ways to reduce your expenses.

4. Record Total (Income Minus Expenses)

Once you have allocated your income towards your expenses, you can calculate your total. This is simply the difference between your income and your expenses. If your total is positive, you have money left over each month. If your count is negative, you are spending more than you earn.

A positive total is a good thing, as it means you have money left over each month to save or invest.

However, if your total is negative, you will need to find ways to reduce your expenses or increase your income. Otherwise, you will quickly find yourself in debt.

FAQ

Does A Budgeting Family Have To Live Together?

No, a family does not have to live together to budget. However, it can be helpful to live together to track expenses more easily.

Who Can Help Me With Budgeting?

Several people can help you with budgeting, including a financial planning association, an accountant, or even family and friends. If your family finances need tidying and having trouble creating a budget, reach out to someone who can help you.

What Is The Average Family Budget?

There is no such thing as an “average” family budget, as every family’s income and expenses vary. However, many budgeting tools and resources are available that can help you create adequate family budgets.

How Often Should I Check My Bank Account Statements?

You should check your bank statements and pay stubs at least once a month to ensure no errors and that you are not going overboard with unnecessary expenses. If you find that you are overspending, you may want to consider creating a budget.

How Much Should I Budget For An Emergency Fund?

Most experts recommend that you budget for an emergency fund that is equal to at least three to six months of your living expenses. This will help ensure that you have enough money to cover unexpected expenses, such as a medical emergency or job loss.

Summary

Congratulations, you have made it to the end!

You now know the basics of how to easily create and manage a family budget. Follow these four simple steps and you will be on your way to saving money and conquering your financial family goals.

Remember, managing money and budgeting is not about deprivation – it’s about having control over your spending and ensuring that your hard-earned money is working for you.

So what are you waiting for?

Get started today!

What type of budget will you use, softcopy or hardcopy?

If softcopy, will you make it easier by using Personal Capital?

Hello! I'm Charles. 1st gen millionaire, real estate investor, health enthusiast, and military veteran. In the last 17 years, I have managed billions of dollars of resources for the Department of Defense. Created financial management plans that enabled fellow service members to get out of thousands of dollars in debt and tailored wellness plans that helped people reverse and eliminate high-blood pressure, pre-diabetes, and obesity. Learn more about me here.